Asked by Fun & Useful on May 18, 2024

Verified

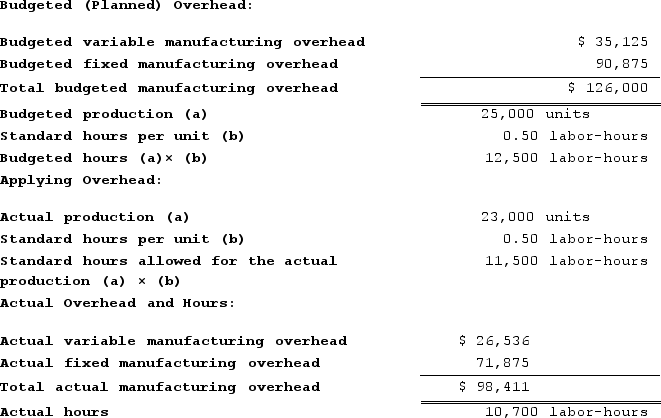

Warrenfeltz Incorporated makes a single product--a cooling coil used in commercial refrigerators. The company has a standard cost system in which it applies overhead to this product based on the standard labor-hours allowed for the actual output of the period. Data concerning the most recent year appear below:

Required:

Required:

a. Compute the variable component of the company's predetermined overhead rate.

b. Compute the fixed component of the company's predetermined overhead rate.

c. Compute the company's predetermined overhead rate.

d. Determine the variable overhead rate variance for the year.

e. Determine the variable overhead efficiency variance for the year.

f. Determine the fixed overhead budget variance for the year.

g. Determine the fixed overhead volume variance for the year.

Variable Component

The portion of a cost or expense that varies directly with the level of production or business activity.

Fixed Component

The part of cost or expense that remains constant in total regardless of fluctuations in the level of activity or volume.

Predetermined Overhead Rate

An estimated rate used to allocate manufacturing overhead costs to individual products or job orders, calculated at the beginning of an accounting period.

- Estimate numerous variances pertinent to manufacturing overhead, like budget, volume, rate, and efficiency variances.

- Analyze the components of a predetermined overhead rate and its calculation.

Verified Answer

= $2.81 per labor-hour

b. Fixed component of the predetermined overhead rate = $90,875/12,500 labor-hours

= $7.27 per labor-hour

c. Predetermined overhead rate = $126,000/12,500 labor-hours = $10.08 per labor-hour

d. Variable overhead rate variance = (Actual hours × Actual rate) − (Actual hours × Standard rate)

= ($26,536) − (10,700 labor-hours × $2.81 per labor-hour)

= ($26,536) − ($30,067)

= $3,531 Favorable

e. Variable overhead efficiency variance = (Actual hours − Standard hours) × Standard rate

= (10,700 labor-hours − 11,500 labor-hours) × $2.81 per labor-hour

= (−800 labor-hours) × $2.81 per labor-hour

= $2,248 Favorable

f. Budget variance = Actual fixed overhead − Budgeted fixed overhead

= $71,875 − $90,875 = $19,000 Favorable

g. Volume variance = Budgeted fixed overhead − Fixed overhead applied to work in process

= $90,875 − ($7.27 per labor-hour × 11,500 labor-hours)

= $90,875 − ($83,605)

= $7,270 Unfavorable

Learning Objectives

- Estimate numerous variances pertinent to manufacturing overhead, like budget, volume, rate, and efficiency variances.

- Analyze the components of a predetermined overhead rate and its calculation.

Related questions

Emanuele Incorporated Makes a Single Product--A Critical Part Used in ...

Held Incorporated Makes a Single Product--An Electrical Motor Used in ...

Modine Corporation Has Provided the Following Data for September ...

Hykes Corporation's Manufacturing Overhead Includes $5 ...

Wangerin Corporation Applies Overhead to Products Based on Machine-Hours ...