PL

Pamela Lewis

Answers (6)

PL

Answered

The SML shifts:

A) indicate an acceptance of beta.

B) parallel to itself in response to changes in the risk-free rate.

C) and rotates around its horizontal intercept.

D) accommodates a decrease in the risk free rate.

A) indicate an acceptance of beta.

B) parallel to itself in response to changes in the risk-free rate.

C) and rotates around its horizontal intercept.

D) accommodates a decrease in the risk free rate.

On Jul 03, 2024

B

PL

Answered

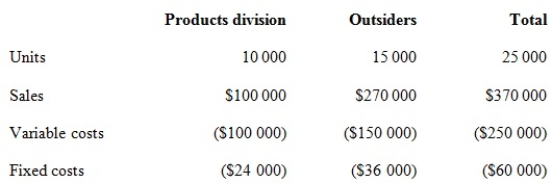

Corporate policy at Weber Pty Ltd requires that all transfers between divisions be recorded at variable cost as a transfer price. Divisional managers have complete autonomy in choosing their sources of customers and suppliers. The Milling Division sells a product called RK2. Forty per cent of the sales of RK2 are to the Products Division, while the remainder of the sales are to outside customers. The manager of the Milling Division is evaluating a special offer from an outside customer for 10 000 units of RK2 at a per unit price of $15.00. If the special offer were accepted, the Milling Division would be unable to supply those units to the Products Division. The Products Division could purchase those units from another supplier for $17 per unit. Annual capacity for the Milling Division is 25 000 units. The 2014 budget information for the Milling Division, based on full capacity, is presented below.

Assume that demand increases for the Milling Division. All 25 000 units can be sold at the regular price to outside customers and the Product Division's annual demand declines to 5000 units. What transfer price would be calculated under the general transfer-pricing formula?

A) $18.00

B) $17.00

C) $16.00

D) $10.00

Assume that demand increases for the Milling Division. All 25 000 units can be sold at the regular price to outside customers and the Product Division's annual demand declines to 5000 units. What transfer price would be calculated under the general transfer-pricing formula?

A) $18.00

B) $17.00

C) $16.00

D) $10.00

On Jul 01, 2024

A

PL

Answered

In a partnership,are partners liable for the crimes committed by another partner? Explain.

On Jun 03, 2024

When a partner commits a crime in the course and scope of transacting partnership business,rarely are his partners criminally liable.But when the partners have participated in the criminal act or authorized its commission,they are liable.They may also be liable when they know of a partner's criminal tendencies yet place him in a position in which he may commit a crime.Until recent times,a partnership could not be held liable for a crime in most states because it was not viewed as a legal entity.However,modern criminal codes usually define a partnership as a "person" that may commit a crime when a partner,acting within the scope of his authority,engages in a criminal act.

PL

Answered

Which of the following is not a characteristic of common stock ownership?

A) residual claimant

B) unlimited liability

C) voting rights

D) right to any dividend paid by the corporation.

A) residual claimant

B) unlimited liability

C) voting rights

D) right to any dividend paid by the corporation.

On Jun 01, 2024

B

PL

Answered

Under the assumptions of the Fisher effect and monetary neutrality, if the money supply growth rate rises, then

A) both the nominal and the real interest rate rise.

B) neither the nominal nor the real interest rate rise.

C) the nominal interest rate rises, but the real interest rate does not.

D) the real interest rate rises, but the nominal interest rate does not.

A) both the nominal and the real interest rate rise.

B) neither the nominal nor the real interest rate rise.

C) the nominal interest rate rises, but the real interest rate does not.

D) the real interest rate rises, but the nominal interest rate does not.

On May 03, 2024

C

PL

Answered

The price faced by a perfectly competitive firm is

A) determined by market demand and supply.

B) the same as the market demand curve.

C) the same as the market supply curve.

D) the same as the firm's marginal cost curve.

A) determined by market demand and supply.

B) the same as the market demand curve.

C) the same as the market supply curve.

D) the same as the firm's marginal cost curve.

On May 02, 2024

A