VE

Vanessa Escalera

Answers (4)

VE

Answered

In order to be relevant to a decision, cost or benefit information must involve ________, rather than ________.

A) a past event; a future event

B) actual data; estimated data

C) a future event; a past event

D) a past event; a current event

A) a past event; a future event

B) actual data; estimated data

C) a future event; a past event

D) a past event; a current event

On Jun 18, 2024

C

VE

Answered

Which of the following statements is accurate?

A) A project that just breaks even on an accounting basis will not pay back.

B) A project that just breaks even on an accounting basis will have a positive rate of return.

C) A project cannot earn a positive return unless its payback period is longer than the project life.

D) If the net income from a project is zero, then the project will have a discounted payback that is equal to its regular payback.

E) The relation between project life and payback period alone cannot tell you whether a project has a positive or negative NPV.

A) A project that just breaks even on an accounting basis will not pay back.

B) A project that just breaks even on an accounting basis will have a positive rate of return.

C) A project cannot earn a positive return unless its payback period is longer than the project life.

D) If the net income from a project is zero, then the project will have a discounted payback that is equal to its regular payback.

E) The relation between project life and payback period alone cannot tell you whether a project has a positive or negative NPV.

On Jun 15, 2024

E

VE

Answered

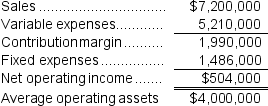

Wolley Inc.reported the following results from last year's operations:  At the beginning of this year, the company has a $1,200,000 investment opportunity with the following characteristics:

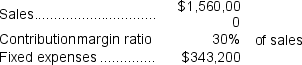

At the beginning of this year, the company has a $1,200,000 investment opportunity with the following characteristics:  The company's minimum required rate of return is 14%.

The company's minimum required rate of return is 14%.

Required:

1.What was last year's margin? (Round to the nearest 0.1%.)

2.What was last year's turnover? (Round to the nearest 0.01.)

3.What was last year's return on investment (ROI)? (Round to the nearest 0.1%.)

4.What is the margin related to this year's investment opportunity? (Round to the nearest 0.1%.)

5.What is the turnover related to this year's investment opportunity? (Round to the nearest 0.01.)

6.What is the ROI related to this year's investment opportunity? (Round to the nearest 0.1%.)

7.If the company pursues the investment opportunity and otherwise performs the same as last year, what will be the overall margin this year? (Round to the nearest 0.1%.)

8.If the company pursues the investment opportunity and otherwise performs the same as last year, what will be the overall turnover this year? (Round to the nearest 0.01.)

9.If the company pursues the investment opportunity and otherwise performs the same as last year, what will be the overall ROI will this year? (Round to the nearest 0.1%.)

10.If Westerville's chief executive officer earns a bonus only if the ROI for this year exceeds the ROI for last year, would the CEO pursue the investment opportunity? Would the owners of the company want the CEO to pursue the investment opportunity?

At the beginning of this year, the company has a $1,200,000 investment opportunity with the following characteristics: The company's minimum required rate of return is 14%.Required:

1.What was last year's margin? (Round to the nearest 0.1%.)

2.What was last year's turnover? (Round to the nearest 0.01.)

3.What was last year's return on investment (ROI)? (Round to the nearest 0.1%.)

4.What is the margin related to this year's investment opportunity? (Round to the nearest 0.1%.)

5.What is the turnover related to this year's investment opportunity? (Round to the nearest 0.01.)

6.What is the ROI related to this year's investment opportunity? (Round to the nearest 0.1%.)

7.If the company pursues the investment opportunity and otherwise performs the same as last year, what will be the overall margin this year? (Round to the nearest 0.1%.)

8.If the company pursues the investment opportunity and otherwise performs the same as last year, what will be the overall turnover this year? (Round to the nearest 0.01.)

9.If the company pursues the investment opportunity and otherwise performs the same as last year, what will be the overall ROI will this year? (Round to the nearest 0.1%.)

10.If Westerville's chief executive officer earns a bonus only if the ROI for this year exceeds the ROI for last year, would the CEO pursue the investment opportunity? Would the owners of the company want the CEO to pursue the investment opportunity?

On May 19, 2024

1.Last year's Margin = Net operating income ÷ Sales = $504,000 ÷ $7,200,000 = 7.0%

2.Last year's Turnover = Sales ÷ Average operating assets = $7,200,000 ÷ $4,000,000 = 1.80

3.Last year's ROI = Net operating income ÷ Average operating assets = $504,000 ÷ $4,000,000 = 12.6%

or

ROI = Margin × Turnover = 7.0% × 1.80 = 12.6%

4.The margin for this year's investment opportunity is: Margin = Net operating income ÷ Sales = $124,800 ÷ $1,560,000 = 8.0%

Margin = Net operating income ÷ Sales = $124,800 ÷ $1,560,000 = 8.0%

5.The turnover for this year's investment opportunity is:

Turnover = Sales ÷ Average operating assets = $1,560,000 ÷ $1,200,000 = 1.30

6.The ROI for this year's investment opportunity is:

ROI = Net operating income ÷ Average operating assets = $124,800 ÷ $1,200,000 = 10.4%

or

ROI = Margin × Turnover = 8.0% × 1.30 = 10.4%

7.If the company pursues the investment opportunity and otherwise performs the same as last year, the margin will be:

Net operating income = $504,000 + $124,800 = $628,800

Sales = $7,200,000 + $1,560,000 = $8,760,000

Margin = Net operating income ÷ Sales = $628,800 ÷ $8,760,000 = 7.2%

8.If the company pursues the investment opportunity and otherwise performs the same as last year, the turnover will be:

Sales = $7,200,000 + $1,560,000 = $8,760,000

Average operating assets = $4,000,000 + $1,200,000 = $5,200,000

Turnover = Sales ÷ Average operating assets = $8,760,000 ÷ $5,200,000 = 1.68

9.If the company pursues the investment opportunity and otherwise performs the same as last year, the ROI will be:

ROI = Net operating income ÷ Average operating assets = $628,800 ÷ $5,200,000 = 12.1%

or

ROI = Margin × Turnover = 7.2% × 1.68 = 12.1%

10.The CEO would not pursue the investment opportunity because it decreases the overall ROI.The owners of the company would not want the CEO to pursue the investment opportunity because its ROI is less than the company's minimum required rate of return.

2.Last year's Turnover = Sales ÷ Average operating assets = $7,200,000 ÷ $4,000,000 = 1.80

3.Last year's ROI = Net operating income ÷ Average operating assets = $504,000 ÷ $4,000,000 = 12.6%

or

ROI = Margin × Turnover = 7.0% × 1.80 = 12.6%

4.The margin for this year's investment opportunity is:

Margin = Net operating income ÷ Sales = $124,800 ÷ $1,560,000 = 8.0%5.The turnover for this year's investment opportunity is:

Turnover = Sales ÷ Average operating assets = $1,560,000 ÷ $1,200,000 = 1.30

6.The ROI for this year's investment opportunity is:

ROI = Net operating income ÷ Average operating assets = $124,800 ÷ $1,200,000 = 10.4%

or

ROI = Margin × Turnover = 8.0% × 1.30 = 10.4%

7.If the company pursues the investment opportunity and otherwise performs the same as last year, the margin will be:

Net operating income = $504,000 + $124,800 = $628,800

Sales = $7,200,000 + $1,560,000 = $8,760,000

Margin = Net operating income ÷ Sales = $628,800 ÷ $8,760,000 = 7.2%

8.If the company pursues the investment opportunity and otherwise performs the same as last year, the turnover will be:

Sales = $7,200,000 + $1,560,000 = $8,760,000

Average operating assets = $4,000,000 + $1,200,000 = $5,200,000

Turnover = Sales ÷ Average operating assets = $8,760,000 ÷ $5,200,000 = 1.68

9.If the company pursues the investment opportunity and otherwise performs the same as last year, the ROI will be:

ROI = Net operating income ÷ Average operating assets = $628,800 ÷ $5,200,000 = 12.1%

or

ROI = Margin × Turnover = 7.2% × 1.68 = 12.1%

10.The CEO would not pursue the investment opportunity because it decreases the overall ROI.The owners of the company would not want the CEO to pursue the investment opportunity because its ROI is less than the company's minimum required rate of return.

VE

Answered

Organizational design is the process of choosing and implementing organizational structures that best arrange resources to accomplish the organization's mission and objectives.

On May 16, 2024

True