Asked by Waseem Nazir on Apr 25, 2024

Verified

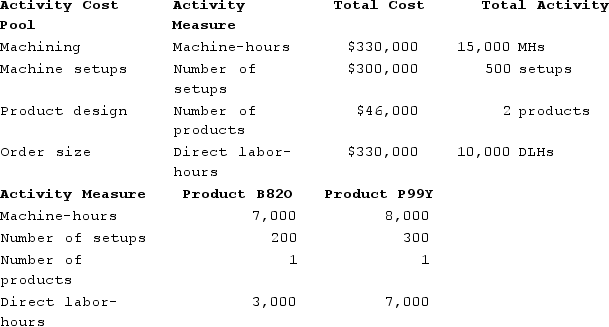

Immen Corporation manufactures two products: Product B82O and Product P99Y. The company uses a plantwide overhead rate based on direct labor-hours. It is considering implementing an activity-based costing (ABC) system that allocates its manufacturing overhead to four cost pools. The following additional information is available for the company as a whole and for Products B82O and P99Y.  Using the ABC system, how much total manufacturing overhead cost would be assigned to Product B82O?

Using the ABC system, how much total manufacturing overhead cost would be assigned to Product B82O?

A) $503,000

B) $297,000

C) $396,000

D) $99,000

Activity-based Costing

An accounting method that assigns costs to products or services based on the resources they consume.

- Calculate the allocation of overhead costs to individual products utilizing the activity-based costing methodology.

- Assess the outcome of utilizing an ABC system on the assignment of manufacturing overhead costs to various products.

Verified Answer

JR

Jessica Rodrigues1 week ago

Final Answer :

C

Explanation :

To determine the manufacturing overhead cost assigned to Product B82O using the ABC system, we need to use the following formula:

Manufacturing overhead cost for Product B82O = (Activity rate for each cost pool x amount of cost driver that each product uses for that cost pool) for all four cost pools

Firstly, we need to calculate the activity rates for each cost pool:

- Activity rate for activity 1: $126,000 ÷ 10,500 = $12 per inspection hour

- Activity rate for activity 2: $231,000 ÷ 7,700 = $30 per machine hour

- Activity rate for activity 3: $525,000 ÷ 35,000 = $15 per direct labor-hour

- Activity rate for activity 4: $364,000 ÷ 8,000 = $45.50 per packaging order

Next, we need to determine how much of each cost driver each product uses for each activity:

- Product B82O uses 2,100 inspection hours, 3,500 machine hours, 2,100 direct labor-hours, and 1,400 packaging orders.

- Product P99Y uses 700 inspection hours, 1,400 machine hours, 7,000 direct labor-hours, and 700 packaging orders.

Using the activity rates and amounts of cost drivers for each product, we can calculate the manufacturing overhead cost assigned to Product B82O as follows:

- Activity 1 cost: $12 x 2,100 = $25,200

- Activity 2 cost: $30 x 3,500 = $105,000

- Activity 3 cost: $15 x 2,100 = $31,500

- Activity 4 cost: $45.50 x 1,400 = $63,700

- Total manufacturing overhead cost for Product B82O: $25,200 + $105,000 + $31,500 + $63,700 = $225,400

Therefore, the total manufacturing overhead cost assigned to Product B82O using the ABC system is $396,000 (Option C).

Manufacturing overhead cost for Product B82O = (Activity rate for each cost pool x amount of cost driver that each product uses for that cost pool) for all four cost pools

Firstly, we need to calculate the activity rates for each cost pool:

- Activity rate for activity 1: $126,000 ÷ 10,500 = $12 per inspection hour

- Activity rate for activity 2: $231,000 ÷ 7,700 = $30 per machine hour

- Activity rate for activity 3: $525,000 ÷ 35,000 = $15 per direct labor-hour

- Activity rate for activity 4: $364,000 ÷ 8,000 = $45.50 per packaging order

Next, we need to determine how much of each cost driver each product uses for each activity:

- Product B82O uses 2,100 inspection hours, 3,500 machine hours, 2,100 direct labor-hours, and 1,400 packaging orders.

- Product P99Y uses 700 inspection hours, 1,400 machine hours, 7,000 direct labor-hours, and 700 packaging orders.

Using the activity rates and amounts of cost drivers for each product, we can calculate the manufacturing overhead cost assigned to Product B82O as follows:

- Activity 1 cost: $12 x 2,100 = $25,200

- Activity 2 cost: $30 x 3,500 = $105,000

- Activity 3 cost: $15 x 2,100 = $31,500

- Activity 4 cost: $45.50 x 1,400 = $63,700

- Total manufacturing overhead cost for Product B82O: $25,200 + $105,000 + $31,500 + $63,700 = $225,400

Therefore, the total manufacturing overhead cost assigned to Product B82O using the ABC system is $396,000 (Option C).

Learning Objectives

- Calculate the allocation of overhead costs to individual products utilizing the activity-based costing methodology.

- Assess the outcome of utilizing an ABC system on the assignment of manufacturing overhead costs to various products.

Related questions

Bertsche Enterprises Makes a Variety of Products That It Sells ...

Immen Corporation Manufactures Two Products: Product B82O and Product P99Y ...

Hane Corporation Uses the Following Activity Rates from Its Activity-Based ...

Weldon Corporation Has Provided the Following Data from Its Activity-Based ...

Thingvold, Inc ...