Asked by Sydney Mankin on Jul 11, 2024

Verified

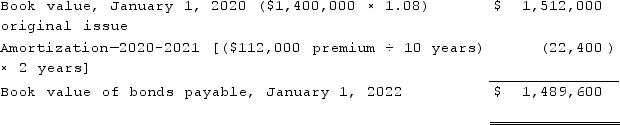

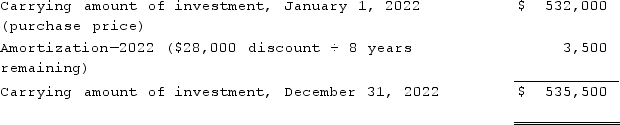

Fargus Corporation owned 51% of the voting common stock of Sanatee, Inc. The parent's interest was acquired several years ago on the date that the subsidiary was formed. Consequently, no goodwill or other allocation was recorded in connection with the acquisition price. On January 1, 2020, Sanatee sold $1,400,000 in ten-year bonds to the public at 108. The bonds pay a 10% interest rate every December 31. Fargus acquired 40% of these bonds on January 1, 2022, for 95% of the face value. Both companies utilized the straight-line method of amortization.What balances would need to be considered in order to prepare the consolidation entry in connection with these intra-entity bonds at December 31, 2022, the end of the first year of the intra-entity investment? Prepare schedules to show numerical answers for balances that would be needed for the entry.

Straight-Line Method

An accounting method of depreciation where an asset's cost is evenly spread over its useful life.

Intra-Entity

Referring to transactions or activities that occur within the same legal entity or among different units of the same corporation.

Ten-Year Bonds

Long-term debt securities issued by entities, maturing in ten years, and often used to raise capital.

- Execute computational analysis and detect entries for consolidation in the context of bond transactions within a singular entity.

Verified Answer

ST

Stephanie TabulaJul 11, 2024

Final Answer :

Carrying amount of bonds payable, January 1, 2022  Carrying amount of 40% of bonds payable (intra-entity portion) , January 1, 2022 = $ 595,840Gain on retirement of bonds, January 1, 2022:

Carrying amount of 40% of bonds payable (intra-entity portion) , January 1, 2022 = $ 595,840Gain on retirement of bonds, January 1, 2022:  Carrying amount of investment, December 31, 2022

Carrying amount of investment, December 31, 2022

Carrying amount of 40% of bonds payable (intra-entity portion) December 31, 2022 ($595,840 − 4,480 premium amortization) = $591,360Carrying amount of investment, December 31, 2022

Carrying amount of 40% of bonds payable (intra-entity portion) December 31, 2022 ($595,840 − 4,480 premium amortization) = $591,360Carrying amount of investment, December 31, 2022

Carrying amount of 40% of bonds payable (intra-entity portion) , January 1, 2022 = $ 595,840Gain on retirement of bonds, January 1, 2022: Carrying amount of investment, December 31, 2022 Carrying amount of 40% of bonds payable (intra-entity portion) December 31, 2022 ($595,840 − 4,480 premium amortization) = $591,360Carrying amount of investment, December 31, 2022

Learning Objectives

- Execute computational analysis and detect entries for consolidation in the context of bond transactions within a singular entity.