JR

Juancho Reynal

Answers (7)

JR

Answered

Which capital investment evaluation technique is described by the following characteristics? (1) Easy to understand and communicate; (2) May result in multiple answers; (3) May lead to incorrect decisions when applied to mutually exclusive investments.

A) NPV.

B) IRR.

C) AAR.

D) Payback period.

E) Discounted payback.

A) NPV.

B) IRR.

C) AAR.

D) Payback period.

E) Discounted payback.

On Jul 07, 2024

B

JR

Answered

A taxpayer may become ineligible for earned income credit if he/she has excessive disqualified income such as dividends or interest.

On Jul 02, 2024

True

JR

Answered

The Lorenz curve shows the distribution of

A) wealth.

B) income.

C) poverty.

D) jobs.

E) unemployment.

A) wealth.

B) income.

C) poverty.

D) jobs.

E) unemployment.

On Jun 07, 2024

B

JR

Answered

Conflicts within a supply chain tend to be more pronounced when the members are part of a corporate vertical marketing system.

On Jun 02, 2024

False

JR

Answered

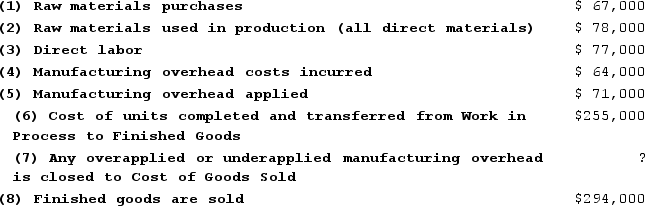

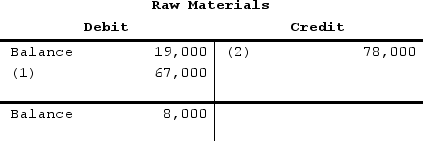

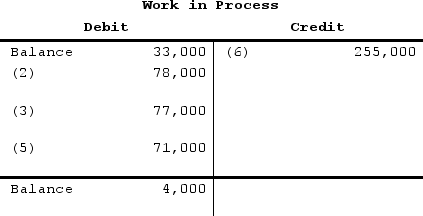

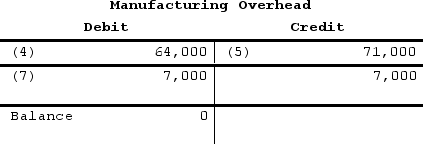

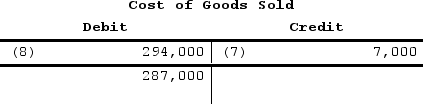

Prahm Incorporated has provided the following data for August:

Transactions:

Transactions:

Required:Complete the following T-accounts by recording the beginning balances and each of the transactions listed above.

Required:Complete the following T-accounts by recording the beginning balances and each of the transactions listed above.

Transactions: Required:Complete the following T-accounts by recording the beginning balances and each of the transactions listed above.On May 08, 2024

<div style=" display: inline-block; vertical-align: top;">

</div> <div style=" display: inline-block; vertical-align: top;">

</div> <div style=" display: inline-block; vertical-align: top;">

</div> <div style=" display: inline-block; vertical-align: top;">

</div> <div style=" display: inline-block; vertical-align: top;">

</div> <div style=" display: inline-block; vertical-align: top;">

</div> <div style=" display: inline-block; vertical-align: top;">

</div> <div style=" display: inline-block; vertical-align: top;">

</div> <div style=" display: inline-block; vertical-align: top;">

</div>

</div>

</div> <div style=" display: inline-block; vertical-align: top;"> </div> <div style=" display: inline-block; vertical-align: top;"> </div> <div style=" display: inline-block; vertical-align: top;"> </div> <div style=" display: inline-block; vertical-align: top;"> </div>JR

Answered

Landon Company developed the following information for 2014: Selling and Administrative Expenses

Variable $30,000 Fixed $50,000 Units in beginning inventory −0− Units sold 26,000 Direct materials used $65,000 Direct labor $105,000 Units produced 30,000 Manufacturing overhead Variable $40,000 Fixed $90,000\begin{array}{lr}\quad \text { Variable } & \$ 30,000 \\\text { Fixed } & \$ 50,000 \\\text { Units in beginning inventory } & -0- \\\text { Units sold } & 26,000 \\\text { Direct materials used } & \$ 65,000 \\\text { Direct labor } & \$ 105,000 \\\text { Units produced } & 30,000 \\\text { Manufacturing overhead } & \\\quad \text { Variable } & \$ 40,000 \\\quad \text { Fixed } & \$ 90,000\end{array} Variable Fixed Units in beginning inventory Units sold Direct materials used Direct labor Units produced Manufacturing overhead Variable Fixed $30,000$50,000−0−26,000$65,000$105,00030,000$40,000$90,000 Instructions

Answer the following questions.

(a) What would be the amount of the cost of goods sold under the absorption costing approach?

(b) What would be the cost of the ending inventory under the variable costing approach?

(c) Which approach would show the greater income for 2014 and by how much?

Variable $30,000 Fixed $50,000 Units in beginning inventory −0− Units sold 26,000 Direct materials used $65,000 Direct labor $105,000 Units produced 30,000 Manufacturing overhead Variable $40,000 Fixed $90,000\begin{array}{lr}\quad \text { Variable } & \$ 30,000 \\\text { Fixed } & \$ 50,000 \\\text { Units in beginning inventory } & -0- \\\text { Units sold } & 26,000 \\\text { Direct materials used } & \$ 65,000 \\\text { Direct labor } & \$ 105,000 \\\text { Units produced } & 30,000 \\\text { Manufacturing overhead } & \\\quad \text { Variable } & \$ 40,000 \\\quad \text { Fixed } & \$ 90,000\end{array} Variable Fixed Units in beginning inventory Units sold Direct materials used Direct labor Units produced Manufacturing overhead Variable Fixed $30,000$50,000−0−26,000$65,000$105,00030,000$40,000$90,000 Instructions

Answer the following questions.

(a) What would be the amount of the cost of goods sold under the absorption costing approach?

(b) What would be the cost of the ending inventory under the variable costing approach?

(c) Which approach would show the greater income for 2014 and by how much?

On May 03, 2024

Absorption Costing Variable Costing Direct materials. $65,000$65,000 Direct labor 105,000105,000 Variable manufacturing overhead. 40,00040,000 Fixed manufacturing overhead. 90,000 - Total manufacturing costs incurred $300,000$210,000 Production in units$30,000$210,000 Production unit cost $10$7\begin{array}{lcc}&\text { Absorption Costing}&\text { Variable Costing }\\\text { Direct materials. } &\$ 65,000&\$ 65,000\\\text { Direct labor }&105,000&105,000\\ \text { Variable manufacturing overhead. } & 40,000 & 40,000 \\ \text { Fixed manufacturing overhead. } & 90,000 & \text { - } \\ \text { Total manufacturing costs incurred } & \$ 300,000 & \$ 210,000 \\\\\text { Production in units}&\$30,000&\$210,000 \\\text { Production unit cost } & \$ 10&\$7 \\\end{array} Direct materials. Direct labor Variable manufacturing overhead. Fixed manufacturing overhead. Total manufacturing costs incurred Production in units Production unit cost Absorption Costing$65,000105,00040,00090,000$300,000$30,000$10 Variable Costing $65,000105,00040,000 - $210,000$210,000$7 (a) Cost of goods sold under the absorption costing approach would be $260000

(26000 units × $10).

(b) Cost of ending inventory under the variable costing approach would be $28000

(4000 units × $7).

(c) Absorption costing income in 2012 would be greater by $12000 (4000 units × $3).

(26000 units × $10).

(b) Cost of ending inventory under the variable costing approach would be $28000

(4000 units × $7).

(c) Absorption costing income in 2012 would be greater by $12000 (4000 units × $3).

JR

Answered

A revolving credit agreement:

A) is similar to a line of credit except that it is binding on the bank.

B) does not guarantee the availability of funds.

C) requires the lender to pay a commitment fee.

D) Both a& c.

E) All of the above

A) is similar to a line of credit except that it is binding on the bank.

B) does not guarantee the availability of funds.

C) requires the lender to pay a commitment fee.

D) Both a& c.

E) All of the above

On Apr 30, 2024

D