WO

winston oladapo

Answers (6)

WO

Answered

What type of securities fraud occurs when an employee falsifies documents to make it appear as though the company had granted options on certain dates,but the dates are selected after the fact by looking backward for dates on which the stock price was low,thereby falsely inflating the profits of the company?

A) Insider trading

B) Pretexting

C) Defalcation

D) Stock-option backdating

E) A Ponzi scheme

A) Insider trading

B) Pretexting

C) Defalcation

D) Stock-option backdating

E) A Ponzi scheme

On Jul 27, 2024

D

WO

Answered

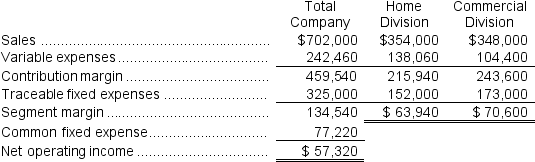

Petteway Corporation has two divisions: Home Division and Commercial Division.The following report is for the most recent operating period:  The common fixed expenses have been allocated to the divisions on the basis of sales.

The common fixed expenses have been allocated to the divisions on the basis of sales.

Required:

a.What is the Home Division's break-even in sales dollars?

b.What is the Commercial Division's break-even in sales dollars?

c.What is the company's overall break-even in sales dollars?

The common fixed expenses have been allocated to the divisions on the basis of sales.Required:

a.What is the Home Division's break-even in sales dollars?

b.What is the Commercial Division's break-even in sales dollars?

c.What is the company's overall break-even in sales dollars?

On Jul 25, 2024

a.Home Division break-even:

a.Home Division break-even:Segment CM ratio = Segment contribution margin ÷ Segment sales

= $215,940 ÷ $354,000 = 0.610

Dollar sales for a segment to break even = Traceable fixed expenses ÷ Segment CM ratio

= $152,000 ÷ 0.610 = $249,180

b.Commercial Division break-even:

Segment CM ratio = Segment contribution margin ÷ Segment sales

= $243,600 ÷ $348,000 = 0.700

Dollar sales for a segment to break even = Traceable fixed expenses ÷ Segment CM ratio

= $173,000 ÷ 0.700 = $247,143

c.The company's overall break-even sales:

CM ratio = Contribution margin ÷ Sales

= $459,540 ÷ $702,000 = 0.655 (rounded)

Total fixed expenses = Total traceable fixed expenses + Common fixed expenses

= $325,000 + $77,220 = $402,220

Dollar sales to break even = Total fixed expenses ÷ CM ratio

= $402,220 ÷ 0.655 = $614,437 (using the unrounded CM ratio)

WO

Answered

How much would the interest rate be if there was no usury law?

On Jun 27, 2024

30%

WO

Answered

Which of Jablin's stages of socialization best describes the stage in which workers adjusts her expectations, resolves organizational conflicts, and develops her own individual job role?

A) anticipatory socialization

B) assimilation

C) exit

D) metamorphosis

A) anticipatory socialization

B) assimilation

C) exit

D) metamorphosis

On Jun 25, 2024

D

WO

Answered

The ______ ______ ______ is an international organization that regulates trade among participating countries and helps importers and exporters conduct their business.

On May 26, 2024

World Trade Organization