Asked by Natalia Portugal on Jul 28, 2024

Verified

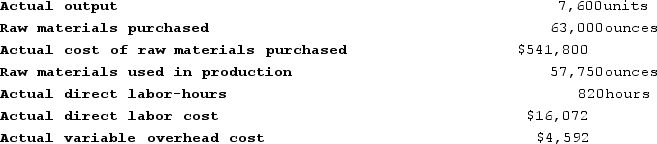

Dirickson Incorporated has provided the following data concerning one of the products in its standard cost system. Variable manufacturing overhead is applied to products on the basis of direct labor-hours.  The company has reported the following actual results for the product for July:

The company has reported the following actual results for the product for July:

The variable overhead efficiency variance for the month is closest to:

The variable overhead efficiency variance for the month is closest to:

A) $336 Favorable

B) $318 Favorable

C) $336 Unfavorable

D) $318 Unfavorable

Variable Overhead

Overhead costs that fluctuate with changes in production level or business activity, such as utilities for machinery.

Efficiency Variance

The difference between the standard cost of labor or materials for actual production and the actual cost incurred, reflecting how efficiently resources are utilized.

Direct Labor-Hours

The total hours worked directly on the production of goods or delivery of services.

- Understand the computation and significance of variable manufacturing overhead variances, including both efficiency and rate variances.

Verified Answer

Actual hours = 4,200

Standard hours = 4,000 (10,000 / 2.5)

Standard rate = $0.08 per DLH

Variable overhead efficiency variance = (4,200 - 4,000) x $0.08 = $16 per hour

Since the actual hours are higher than the standard hours, the variance is unfavorable. Therefore, the closest answer is D, $318 Unfavorable.

Learning Objectives

- Understand the computation and significance of variable manufacturing overhead variances, including both efficiency and rate variances.

Related questions

Ravena Labs ...

Dirickson Incorporated Has Provided the Following Data Concerning One of ...

Bulluck Corporation Makes a Product with the Following Standard Costs ...

Majer Corporation Makes a Product with the Following Standard Costs ...

Puvo, Incorporated, Manufactures a Single Product in Which Variable Manufacturing ...