JM

Jasleen Mahal

Answers (7)

JM

Answered

Chris was driving a car with defective brakes very slowly down Fifth Avenue looking for a parking place. Mindy jumped out into the street five feet in front of his car. Chris could not help but hit her. What is Chris's best defense to the charge of negligence?

A) Mindy had a mental deficiency.

B) He was not negligent since he did not have a statutory duty to keep his brakes in top condition.

C) Mindy crossed in the middle of the street, which is against the law.

D) He was lawfully seeking a parking place and did not see her jump out.

A) Mindy had a mental deficiency.

B) He was not negligent since he did not have a statutory duty to keep his brakes in top condition.

C) Mindy crossed in the middle of the street, which is against the law.

D) He was lawfully seeking a parking place and did not see her jump out.

On Jul 23, 2024

C

JM

Answered

The President counts among his economic advisors the Congressional Budget Office.

On Jul 23, 2024

False

JM

Answered

A highly corrosive liquid that is stored on the property of Acme Waste Disposal leaks from its container and seeps into the foundations of the business next door, badly damaging the building. Acme will be liable only if the injured party can prove Acme was negligent.

On Jul 20, 2024

False

JM

Answered

Followership research is about ______.

A) how and why followers respond to leaders

B) how followers can acquire traits to become leaders

C) challenging the validity of leadership theories

D) helping corporations achieve better bottom line results

A) how and why followers respond to leaders

B) how followers can acquire traits to become leaders

C) challenging the validity of leadership theories

D) helping corporations achieve better bottom line results

On Jun 23, 2024

A

JM

Answered

In which of the following steps of creating employee development plans focuses on who will be involved, what the costs will be, how much time is needed, and what support is needed to ensure success?

A) determine resources

B) identify barriers

C) link competencies and skills to business goals

D) identify learning and development activities

E) assess employees' needs

A) determine resources

B) identify barriers

C) link competencies and skills to business goals

D) identify learning and development activities

E) assess employees' needs

On Jun 20, 2024

A

JM

Answered

Mutual mistake is more likely to make a contract voidable than a unilateral mistake.

On May 24, 2024

True

JM

Answered

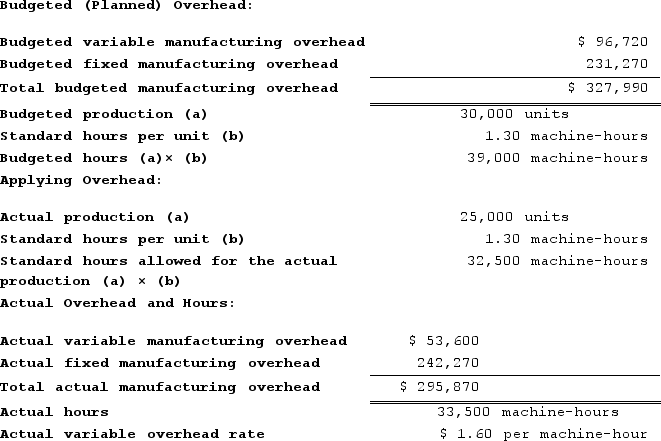

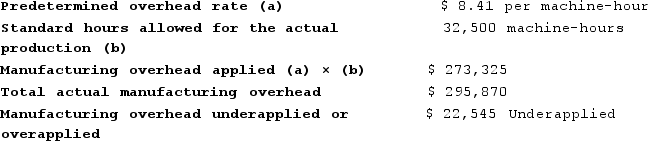

Pickell Incorporated makes a single product--a cooling coil used in commercial refrigerators. The company has a standard cost system in which it applies overhead to this product based on the standard machine-hours allowed for the actual output of the period. Data concerning the most recent year appear below:

Required:

Required:

a. Determine the variable overhead rate variance for the year.

b. Determine the variable overhead efficiency variance for the year.

c. Determine the fixed overhead budget variance for the year.

d. Determine the fixed overhead volume variance for the year.

e. Determine whether overhead was underapplied or overapplied for the year and by how much.

Required:a. Determine the variable overhead rate variance for the year.

b. Determine the variable overhead efficiency variance for the year.

c. Determine the fixed overhead budget variance for the year.

d. Determine the fixed overhead volume variance for the year.

e. Determine whether overhead was underapplied or overapplied for the year and by how much.

On May 21, 2024

a. Variable component of the predetermined overhead rate (Standard rate) = $96,720/39,000 machine-hours

= $2.48 per machine-hour

Variable overhead rate variance = (Actual hours × Actual rate) − (Actual hours × Standard rate)

= ($53,600) − (33,500 machine-hours × $2.48 per machine-hour)

= ($53,600) − ($83,080)

= $29,480 Favorable

b. Labor efficiency variance = (Actual hours − Standard hours) × Standard rate

= (33,500 machine-hours − 32,500 machine-hours) × $2.48 per machine-hour

= (1,000 machine-hours) × $2.48 per machine-hour

= $2,480 Unfavorable

c. Budget variance = Actual fixed overhead − Budgeted fixed overhead

= $242,270 − $231,270 = $11,000 Unfavorable

d. Fixed component of the predetermined overhead rate = $231,270/39,000 machine-hours

= $5.93 per machine-hour

Volume variance = Budgeted fixed overhead − Fixed overhead applied to work in process

= $231,270 − ($5.93 per machine-hour × 32,500 machine-hours)

= $231,270 − ($192,725)

= $38,545 Unfavorable

e. Predetermined overhead rate = $327,990/39,000 machine-hours = $8.41 per machine-hour

= $2.48 per machine-hour

Variable overhead rate variance = (Actual hours × Actual rate) − (Actual hours × Standard rate)

= ($53,600) − (33,500 machine-hours × $2.48 per machine-hour)

= ($53,600) − ($83,080)

= $29,480 Favorable

b. Labor efficiency variance = (Actual hours − Standard hours) × Standard rate

= (33,500 machine-hours − 32,500 machine-hours) × $2.48 per machine-hour

= (1,000 machine-hours) × $2.48 per machine-hour

= $2,480 Unfavorable

c. Budget variance = Actual fixed overhead − Budgeted fixed overhead

= $242,270 − $231,270 = $11,000 Unfavorable

d. Fixed component of the predetermined overhead rate = $231,270/39,000 machine-hours

= $5.93 per machine-hour

Volume variance = Budgeted fixed overhead − Fixed overhead applied to work in process

= $231,270 − ($5.93 per machine-hour × 32,500 machine-hours)

= $231,270 − ($192,725)

= $38,545 Unfavorable

e. Predetermined overhead rate = $327,990/39,000 machine-hours = $8.41 per machine-hour