Asked by Areli Hernandez on Jun 12, 2024

Verified

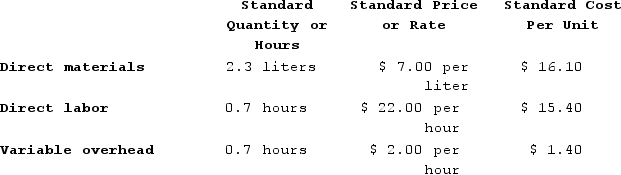

Miguez Corporation makes a product with the following standard costs:  The company budgeted for production of 2,600 units in September, but actual production was 2,500 units. The company used 5,440 liters of direct material and 1,680 direct labor-hours to produce this output. The company purchased 5,800 liters of the direct material at $7.20 per liter. The actual direct labor rate was $24.10 per hour and the actual variable overhead rate was $1.90 per hour.The company applies variable overhead on the basis of direct labor-hours. The direct materials purchases variance is computed when the materials are purchased.The variable overhead rate variance for September is:

The company budgeted for production of 2,600 units in September, but actual production was 2,500 units. The company used 5,440 liters of direct material and 1,680 direct labor-hours to produce this output. The company purchased 5,800 liters of the direct material at $7.20 per liter. The actual direct labor rate was $24.10 per hour and the actual variable overhead rate was $1.90 per hour.The company applies variable overhead on the basis of direct labor-hours. The direct materials purchases variance is computed when the materials are purchased.The variable overhead rate variance for September is:

A) $175 Favorable

B) $168 Unfavorable

C) $168 Favorable

D) $175 Unfavorable

Variable Overhead Rate Variance

The difference between the actual variable overhead incurred and the expected variable overhead based on the predetermined rate.

- Calculate the efficiency variances and rate variances of variable overhead to examine control over overhead costs.

Verified Answer

WT

Warren TubalJun 14, 2024

Final Answer :

C

Explanation :

First, we need to calculate the standard variable overhead rate per direct labor-hour:

Budgeted Variable Overhead Costs / Budgeted Direct Labor-hours

= $3,790 / 2,600 hours

= $1.46 per hour

Next, we can calculate the flexible budget for variable overhead:

Flexible Budget = Actual Direct Labor-hours x Standard Variable Overhead Rate

= 1,680 hours x $1.46 per hour

= $2,455.20

Finally, we can calculate the variable overhead rate variance:

Variable Overhead Rate Variance = Actual Variable Overhead - Flexible Budget

= ($1.90 per hour x 1,680 hours) - $2,455.20

= $3,192 - $2,455.20

= $736.80 unfavorable

Therefore, the correct answer is C) $168 Favorable, which is not one of the answer choices. Since $736.80 unfavorable is not an option, the closest answer choice is C) $168 Favorable, which is the reverse of $168 unfavorable. This means that the actual variable overhead was $168 less than the flexible budget for variable overhead, which is a favorable variance.

Budgeted Variable Overhead Costs / Budgeted Direct Labor-hours

= $3,790 / 2,600 hours

= $1.46 per hour

Next, we can calculate the flexible budget for variable overhead:

Flexible Budget = Actual Direct Labor-hours x Standard Variable Overhead Rate

= 1,680 hours x $1.46 per hour

= $2,455.20

Finally, we can calculate the variable overhead rate variance:

Variable Overhead Rate Variance = Actual Variable Overhead - Flexible Budget

= ($1.90 per hour x 1,680 hours) - $2,455.20

= $3,192 - $2,455.20

= $736.80 unfavorable

Therefore, the correct answer is C) $168 Favorable, which is not one of the answer choices. Since $736.80 unfavorable is not an option, the closest answer choice is C) $168 Favorable, which is the reverse of $168 unfavorable. This means that the actual variable overhead was $168 less than the flexible budget for variable overhead, which is a favorable variance.

Learning Objectives

- Calculate the efficiency variances and rate variances of variable overhead to examine control over overhead costs.

Related questions

Fluegge Incorporated Has Provided the Following Data Concerning One of ...

Miguez Corporation Makes a Product with the Following Standard Costs ...

Kartman Corporation Makes a Product with the Following Standard Costs ...

The Following Standards for Variable Manufacturing Overhead Have Been Established ...

The Following Data Have Been Provided by Furr Corporation ...